Hey, everyone — Crazy fact: our auto industry job board pulled in over 100,000 views last month across our newsletter and website.

The best part? Those views are highly engaged and concentrated within the automotive industry.

Translation: your next hire is probably already looking. So—list your job for FREE now!

—CDG

First time reading the CDG Newsletter? Subscribe here.

There are a lot of factors that go into determining the health of the car market. Vehicle, sales volume, inventory, profit margins—I could go on…

But—believe it or not—what I get asked about most of the time is auto lending.

And I know why. Lending trends usually reveal what’s really going on with typical household finances and often influences consumer appetite for big ticket items—like cars. But beyond knowing where the industry is at now— understanding the lending market better can help dealers, investors, and consumers scenario plan for whatever future lies ahead.

And here’s what the latest trends are showing…

Trend #1: Repossessions are rising—but it’s more of a reset than a red flag.

According to the latest data from Cox Automotive, repossessions went up 23% year-over-year last July and increased 14% from pre-pandemic levels. And recently, the Consumer Financial Protection Bureau came to a similar conclusion—from December 2019 to December 2022, vehicle repossessions rose 22.5% across nine major lenders.

I know—seems like alarm bells should be ringing right?

But we have to put the numbers into context. In 2020–2021, repossessions hit record lows due to government stimulus money, loan deferrals, and lender forbearance programs. The recent uptick is—in part—a ‘normalization’ of the market rather than an uncontrolled spike.

So—it wasn’t too surprising when the analysts and auto finance specialists I spoke to this week told me repossessions are not a big deal… yet.

What’s fueling the optimism?

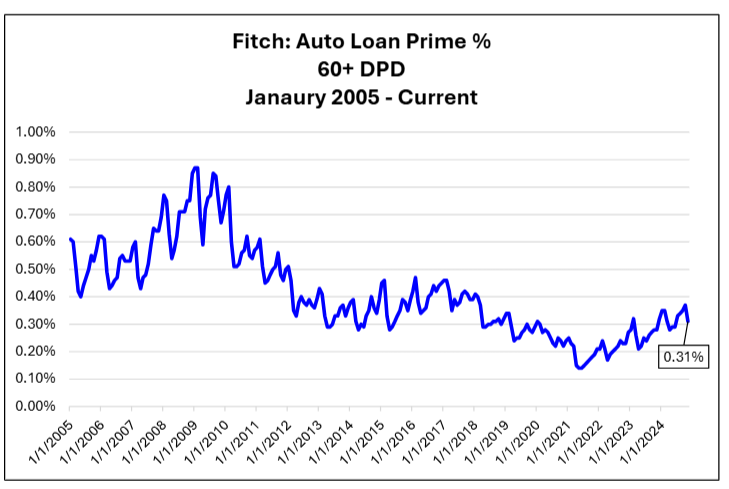

Prime borrowers are not in trouble. Prime auto loans (borrowers with strong credit) account for the majority of auto loan originations, and their delinquency rates have not spiked to concerning levels.

(Source: Fitch Ratings)

The share of subprime loans is the lowest it's been in years. Subprime auto loans (borrowers with weak credit and the most vulnerable to repossession) are not taking out (or being given) as many loans as they once were. Fewer loans = fewer chances for repo.

After years of tightening—auto lenders are slowly opening up credit availability. Unlike the 2008 financial crisis, lenders are not completely shutting off access to auto loans, and there is still liquidity in the market. On top of that—there are lenders out there that are finding new and innovative ways to approve borrowers with poor or no credit history (e.g. Lendbuzz).

All in all—this is good news for the market…

Kenect AI is the platform auto dealers are using to gather reviews, generate leads, and improve their online reputation, all powered by AI!

Did you know that your 1, 2 and 3-star reviews can cost your auto dealership up to 30 leads per day? Kenect AI will help eliminate and remove negative reviews from your online sites such as Google, Meta, Cars.com and more. Kenect also uses AI to respond to reviews and deliver sentiment analysis—in real-time.

Complete an online demo and see why more than 10,000 dealerships in North America use Kenect every day!

EXCLUSIVE OFFER! The first 25 people to complete a demo with Kenect will each receive a $100 Amazon Gift Card!

However, it’s generally cheaper for an auto lender to grant a loan extension rather than repossess the vehicle—which is why…

Trend #2: Loan extensions are keeping subprime borrowers afloat—but at a cost.

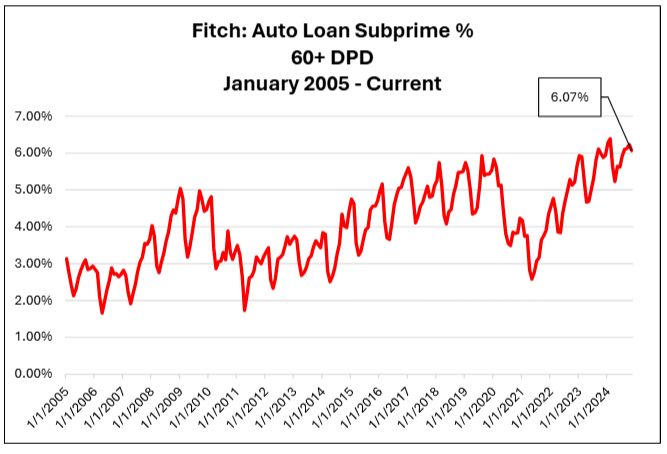

Subprime auto loan delinquencies were near record highs at 6.07% in December (Fitch Ratings), up 86 basis points from 2022. But here’s what’s different—more loans are rolling through late-stage delinquency without going through default and being charged off.

(Data source: Fitch Ratings)

Instead—lenders are keeping borrowers in their loans with payment extensions and modifications. This strategy helps borrowers in the short term—but also traps many in an expensive cycle with no easy way out.

For struggling borrowers, a loan extension is a way to avoid defaulting on their loan. But those skipped payments aren’t erased—they’re tacked onto the end of the loan, and interest keeps accruing.

One analyst I spoke with called it a "bubble that's beginning to grow.”

And the longer a borrower stays in that bubble, the harder it gets to escape.

A two-month extension on a 20% APR loan can add hundreds—if not thousands—of dollars in extra interest.

Some borrowers are extending for 12+ months, paying nothing toward their principal balance and sinking further into negative equity.

For now—this isn’t a Great Financial Crisis-style collapse—but it is changing how dealers, lenders, and consumers navigate auto finance.

More deals could fall apart in the F&I office as subprime approvals tighten, making it harder to sell vehicles to credit-challenged buyers and potentially denting F&I profits.

Lenders offering extensions may be avoiding short-term losses, but they’re also building up long-term risk if these loans fail down the road.

As subprime approvals tighten, many could lose access to car ownership altogether or face incredibly high auto loan rates (30%+ in some cases, according to auto finance expert Bill Ploog).

But for Cox Automotive’s Jeremy Robb–inflation is still a top risk to watch out for...

Trend #3: The Fed’s rate cuts aren’t reaching car buyers—and inflation Isn’t helping.

Everyone knows interest rates are coming down.

But for car buyers? It doesn’t feel like it.

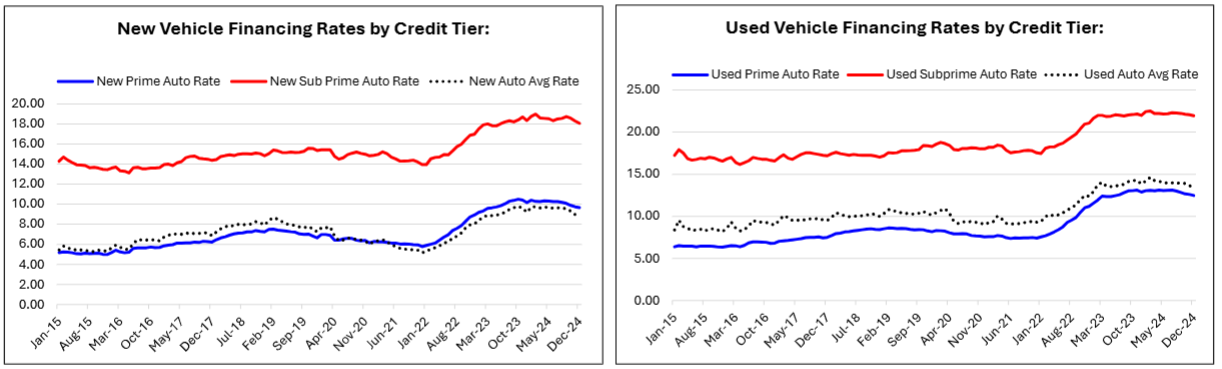

Despite the Fed cutting rates by a full percentage point, auto loan rates actually ticked up in January—hitting 9.25% for new cars and 13.88% for used cars.

(Data source: Dealertrack)

Meanwhile, the cost of simply owning a car keeps climbing:

Insurance costs have surged 44% over the past few years, as more expensive vehicles push premiums higher, per Bankrate.

And maintenance and repairs are up 13-16%, with labor shortages and pricier parts making service bills steeper than ever.

But analysts warn that since many buyers are now expecting prices to drop, they are holding off on purchases—but that hesitation could lead to a deflationary spiral:

Consumers expect prices to fall → they delay purchases → supply builds up → prices drop → more hesitation.

This is exactly the opposite of what the Fed wants—which is why rate cuts aren’t a sure thing.

Looking ahead? Tax refund season could provide a short-term lift, as buyers historically use refunds to cover down payments or pay off existing loans. But don’t expect it to be a game-changer. With inflation still lingering and core expenses eating into household budgets, the Fed is moving cautiously—meaning auto financing probably won’t get dramatically cheaper anytime soon.

Putting it all together—The next few months will be a test of how deep affordability challenges still run. If inflation sticks around, household budgets will stay squeezed, limiting how much relief rate cuts can really provide. And if buyers keep waiting for prices to drop further, dealers and lenders may have to rethink how they structure deals to keep cars moving entirely.

For now, this isn’t a market in crisis—but it’s definitely one in transition. And how the industry responds will determine whether auto finance finally stabilizes—or just shifts into a new kind of uncertainty.

How Cavender built a scalable dealer group—the framework for success

How to run a dealership like a $10B company: Secrets of a Lithia Motors GM

Toyota plans EV, battery push in China and U.S. amid quarterly profit surge.

Markets rise on tariff pause, but earnings disappoint.

Ford exec shuffle puts Andrew Frick over both gas, EV businesses.

Honda, Hyundai, Ford, Subaru, and Kia EV sales climb in January.

EPA freezes grants and threatens to cut over 1,000 jobs.

Did you enjoy this edition of The Breakdown newsletter?

Thanks for reading. See you on the next edition…

—Car Dealership Guy

Want to advertise with CDG? Click here.

Want to be considered as a guest on the CDG podcast? Right this way.

Want to pitch a story for the newsletter? Share it here.