Hey, everyone. We finally did it. We launched our news site, CDG News. It’s your No. 1 (free) resource for unbiased car industry news—written concisely and in plain English. CDG News is a perfect companion for this newsletter, complete with podcast summaries, industry insights, dealership best practices (written by actual dealers), and consumer tips.

Excited to see where this goes.

—CDG

First time reading the CDG Newsletter? Subscribe here.

3 Things to Know About The State of Auto Lending

Believe it or not, the question I get from dealers and automotive professionals most often isn’t whether Tesla is really going to the moon. It’s actually about the auto lending industry.

And I think I know why: Automotive lending is a key indicator of the health of our industry, and understanding it better helps us come a little closer to grasping whatever future lies ahead.

So today, let’s spend some time talking about lending. I’ve got three major, timely things for you to keep in mind re: the current state of auto lending. Let’s get into it →

First: The auto finance market is back to growth mode.

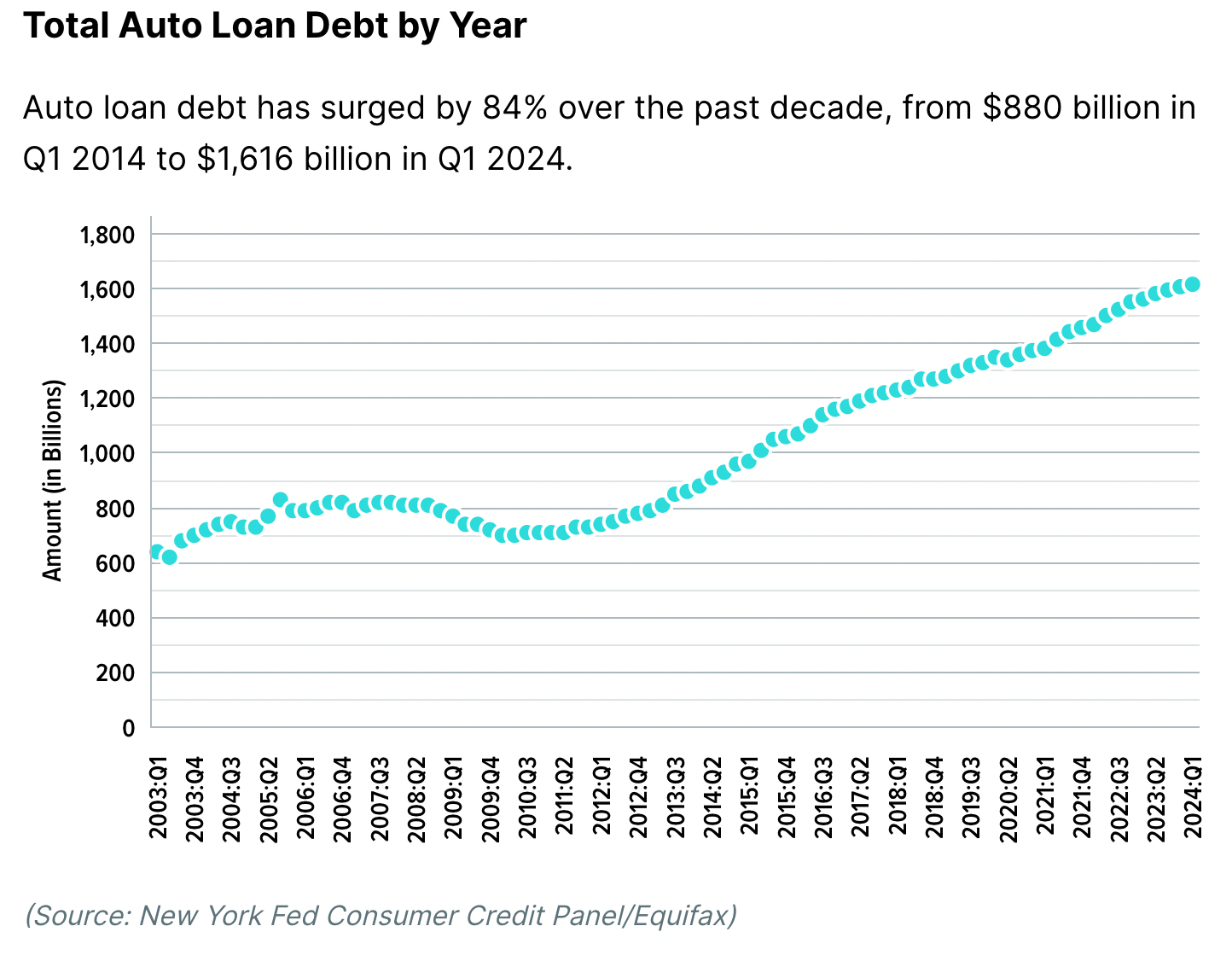

The details: According to new data from Big Wheels, the auto finance market maintained outstandings north of $1.3 trillion (more than the whole GDP of the Netherlands, FYI) in 2023. Auto lending tallied annual growth of 3.7%, bringing it back to an upward trajectory after a 0.6% decline in 2022.

Looking ahead: It seems the upward trajectory is set to stick around—as of Q1 of this year, Americans’ auto loan debt totaled over $1.6 trillion, or about $13,000 per household. It’s a notable reversal of the trend of auto loan rates declining that lasted from the late 1990s through the middle of the Covid-19 pandemic. The reason behind this reversal? The usual suspects…inflation and increasing interest rates.

Via WalletHub

Let’s break down some interesting stats from last year even further…

Leasing: Auto leasing as a percentage of overall outstandings kept on par with recent years, dipping in 2023. Leases accounted for 16.9% of outstandings in 2023, down from 18% in 2022 and 25% in 2019. FYI, leases historically accounted for around 30% of US retail volume pre-pandemic, but they fell to about 15% by the end of 2022 as manufacturers cut back on incentives given high demand and low supply. That said, leasing is finally picking back up again.

Big winners: When it comes to originations, Toyota Financial was still top dog as of 2023. It originated $65.6 billion of loans and leases last year, more than $20 billion ahead of its closest competitor, GM Financial. Chase Auto, Ally, and Ford Credit closed out the top five.

Credit unions: 54 of the top 100 originators were credit unions (which still typically offer lower interest rates, more flexible repayment terms, and more lax credit standards compared to captives). Those 54 had an average growth rate of 1.8% last year, down from 22.2% in 2022. Keep in mind, credit unions went through a major auto loan origination growth spurt post-2021 when auto prices were through the roof and demand was surging.

Something that caught my eye: Four out of the 10 highest originators in 2023 posted annual origination declines. And origination volume shrank for half of the companies within the top 100 last year. Which brings us to this…

Second: Alternative credit is bringing more subprime borrowers into the fold.

Alternative credit, aka credit for borrowers with less-than-ideal credit scores but a steady income and normal debt-to-income ratio, is becoming increasingly popular—new startups appear to be wooing away borrowers from the major lenders and institutions that might otherwise turn them away.

FYI: The latest data from FICO found the national average credit score is 717, down a point from the last reading and the first time the metric has decreased in a decade. This could suggest interest rates and inflation are weighing on consumers.

Important stats here:

More than 28 million Americans have no mainstream credit file at the credit bureaus and are considered “credit invisible.”

21 million more Americans are considered unscorable (often the case when borrowers don't have a credit history or haven’t used credit recently).

And 57 million Americans have scores that put them in the subprime category.

Banks, credit unions, and captive finance typically don’t lend to the above groups given their increased risk of default. And with current default and delinquency rates at a 25-year high of about 6%...some of that apprehension is warranted.

But newcomers and other alternative lenders are leveraging tech to lend to the previously un-lendable. How? Glad you asked…

Third: AI and other new tech is changing the face of lending as we know it.

Lenders that use artificial intelligence can get a much fuller picture of applicants’ identity, income, employment, likelihood of making payments on time, and overall creditworthiness. Basically, AI gives them more info than the typical credit score and bank statement ever could—meaning they can make smarter lending decisions, better assess risk and compliance, and identify customers on the brink of default before they go bust.

Think about it: Credit bureaus were designed without specificity—they’re supposed to serve a wide range of industries and use cases, using often limited data to summarize what are pretty complex circumstances. AI tech can get more specific than that, tapping into financial history, transaction records, credit bureau data, and social media behavior to suss out a borrower's creditworthiness.

But an important reality check: Like any new tech, AI isn’t perfect. Understanding individual consumers in different markets requires different AI training, and experts have said you need 18+ months of data for a credit model to adjust to a new market.

Still, it’s interesting to think about how tech is infiltrating (and will continue to infiltrate) the auto industry, from OEMs (see also: last week’s newsletter) to F&I departments. I’m curious to see how AI-powered borrower analysis changes the share of subprime borrowers in the larger lending pool. What about you?

What’s the secret to building the largest Honda store in the US? Rita Case, CEO of Rick Case Automotive, gave me the full rundown in this awesome episode. We also talked about betting big on small brands, the leasing boom in Florida, and the importance of philanthropy. Don’t miss this one.

These are the most surprising dealership growth hacks, according to Nate Mihalovich, CEO of The Lasso…well, you’ll have to listen to the episode to find out. We also jammed on his journey from a $300 million exit to transforming how dealers buy cars, which retailers pay the most for customer trade-ins, how dealers out-compete Carmax and Carvana, and tons more. Listen to this one!

Listen to the episodes here, and subscribe to the CDG Podcast on Apple, Spotify, or wherever else you get your podcasts. And thank you to Podium, Foureyes, Auto Hauler Exchange, and The Lasso for making these episodes possible.

Move your dealership with Uber for Business. Leverage the largest mobility network in the world to request rides for customers—even if they don’t have the Uber app.

Increase customer satisfaction: Provide on-demand rides with a flexible, familiar platform.

Control costs: Reduce costs associated with loaner and shuttle use. Only pay for rides taken.

Insurance and safety: Uber maintains commercial auto insurance that covers passenger trips on the Uber platform.

Streamline operations: Move people and parts with one dashboard.

Last week, I asked you this question: What do you think about the future of software-defined vehicles?

Hundreds of votes later, here’s what you had to say:

44% of you said they’re over-hyped

30% of you said they’re genius

And the rest? Undecided (you should keep reading CDG to help make up your mind 👀)

Some of my favorite responses you shared?

“Software can't fix everything.”

“This is the biggest disruption in our history, and it’s only the beginning.”

“I enjoy actually driving a car. I may never get rid of my five speed 1997 Wrangler and my six speed 2007 Honda S2000.”

“Automakers have been very slow to adopt prudent software development practices. Instead of taking the best of long-standing best practices from the enterprise software world, they've adopted the worst of the Silicon Valley cellphone app (ship sh*t and fix it later, maybe after the third update) world. The result is unnecessary complexity, shoddy testing, and an unwanted fixation on getting rich selling subscription services.”

We’ve got tons of great jobs hitting the CDG Job Board right now. Here are some standouts for anyone looking for their next move.

HGreg is looking for a senior controller to oversee financial management of its Nissan dealerships in Florida. Big opp for numbers people.

Want to move to Hawaii? Become the marketing coordinator for Orchid Isle Ford in Hilo, Hawaii.

Looking to hire? Add your roles today—it’s 100% free.

The average age of US vehicles? Now a new record at 12.6 years in 2024.

Electricity consumption from US EVs over the first two months of 2024 jumped by over 50% from the same time last year.

Subaru and Toyota are partnering to develop four battery electric SUVs.

Peugeot is partnering with German mobility startup Vay to develop what it calls “teledriving” tech, an alternative to autonomous driving.

GM and its battery suppliers started a $150 million relief fund to reimburse Chevrolet Bolt EV owners whose cars had manufacturing defects.

Thanks for reading. I appreciate your support—have a great day.

—Car Dealership Guy

Did you like this edition of the newsletter?

Want to advertise with CDG? Click here.

Want to be considered as a guest on the CDG podcast? Right this way.

Want to pitch a story for the newsletter? Share it here.