Hey, everyone — New data from AccuTrade shows that most trade-in values for mass-market brands dropped by double-digit percentages against 2023.

No surprise — Toyota held up better than most. Its trade-in values only dipped 8%, while Fiat and Dodge saw drops as steep as 22%.

Why? Toyota’s lean new car supply keeps it from slashing prices or offering big incentives — unlike Dodge, where heavier discounts are dragging down used values too.

—CDG

First time reading the CDG Newsletter? Subscribe here.

Insurance. We all need it. It’s a fundamental part of car ownership. And while car ownership used to be a symbol of financial independence — it’s now turning into a budget burden for many drivers. Between volatile inflation, elevated interest rates, and near-record-high car prices, affording a vehicle feels like a stretch for most.

And just when buyers think they can make the payments… Auto insurance premiums are pumping the brakes — blowing up budgets and, in many cases, even derailing deals entirely.

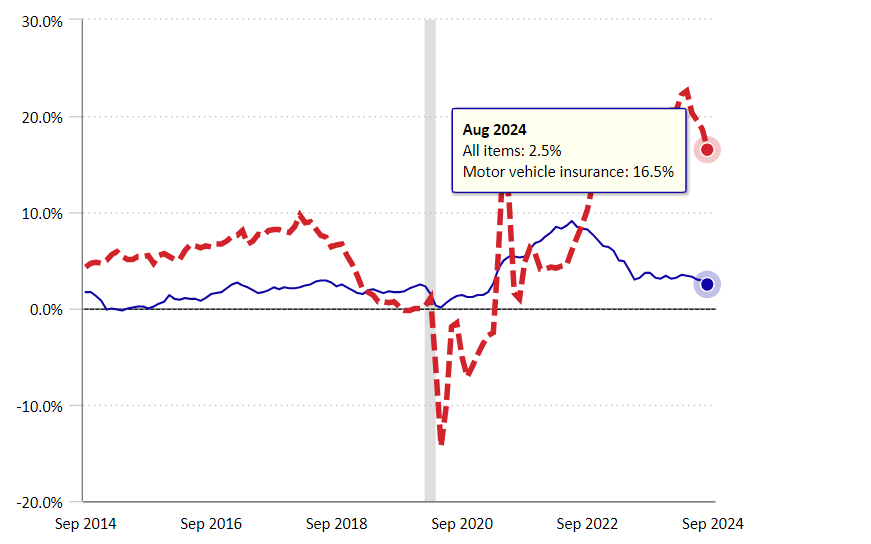

Auto insurance rates have not been trending positively:

The average rate for full auto coverage in the U.S. is set to rise an estimated 22% year-over-year to $2,469 per year in 2024.

Average annual auto policies are now more than $6,000 in some cities, more than three times the national average. (Looking at you, New York…)

And in general, auto insurance rates are rising at a much faster pace compared to overall consumer goods. (See the chart below for the full picture...)

Source: BLS

These days, the Subaru Outback, Honda CR-V, and Honda Pilot are the least expensive car models to insure… while the Tesla Model S Performance, Audi R8 Quattro Performance, and the Tesla Model X are the most expensive cars to insure.

Since 2022, five major factors have driven auto insurance prices higher:

1) Soaring repair costs: Between 2022 and 2023, repair costs shot up by 20.7%, thanks to inflation, supply chain issues, and labor shortages. EV repairs are also more expensive compared to gas-powered cars, driving claim frequency and severity higher.

2) More tech, more problems: Advanced Driver Assistance Systems, sensors, and cameras (you get it) increased the likelihood of newer vehicles being totaled. Claims on totaled vehicles have actually jumped 29% since 2020.

3) An uptick in uninsured motorists (11.1% in 2019 to 14% by 2022) due to more drivers dropping coverage during the pandemic. More accidents with uninsured motorists shift the financial burden to policy holders, pushing premiums even higher.

4) Policyholders who hired more accident attorneys early in the claims process and ended up driving legal expenses and increasing overall claim costs.

5) Frequent extreme weather events, like damages from hurricanes and hailstorms, have caused billions of dollars in damage and have strained insurers with unpredictable payouts.

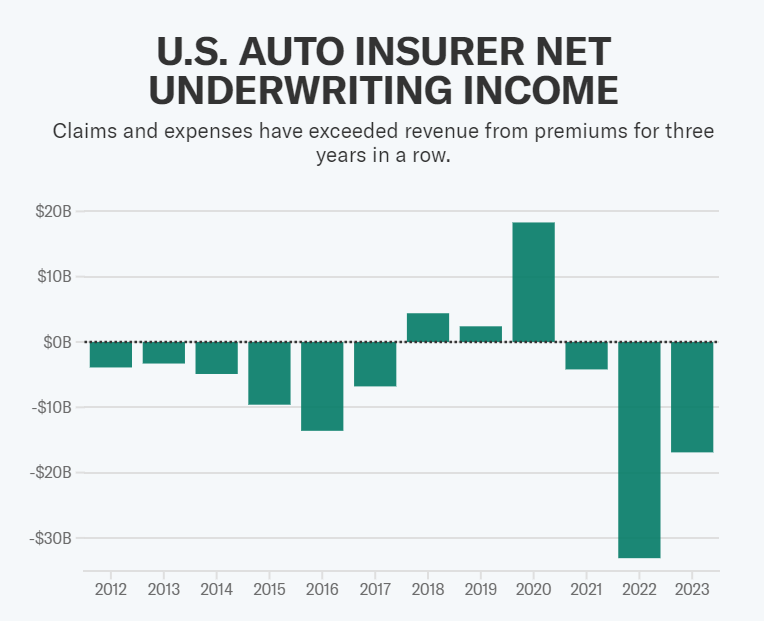

All of this led to the massive underwriting losses auto insurance companies accrued in 2022 – 2023. These losses meant insurance companies paid out more in claims and expenses than they took in through premiums. But there’s more…

Source: AM Best

Auto insurance premiums have reacted slowly to economic changes because insurers must submit rate changes for state approval. Each state has its own process – meaning regulators get flooded with requests from multiple companies, creating a bottleneck. As a result, it can take up to 18 months for new rates to be reviewed and approved.

So – when inflation started ratcheting up over the past three years, premiums were too low to cover rising costs – pressuring insurers to raise rates to keep things stable.

But still — today, insurance companies are still pretty profitable. In 2023, their average profit margin hit 9.5%, up from 4.7% in 2022. And they didn’t just rely on collecting premiums — they also invested it in stocks, bonds, and real estate to grow profits.

However, not everyone has fared well…

Dealers and consumers have been hit hard by rapidly rising insurance premiums.

Rising auto insurance rates are keeping buyers on the sidelines and crushing dealership sales.

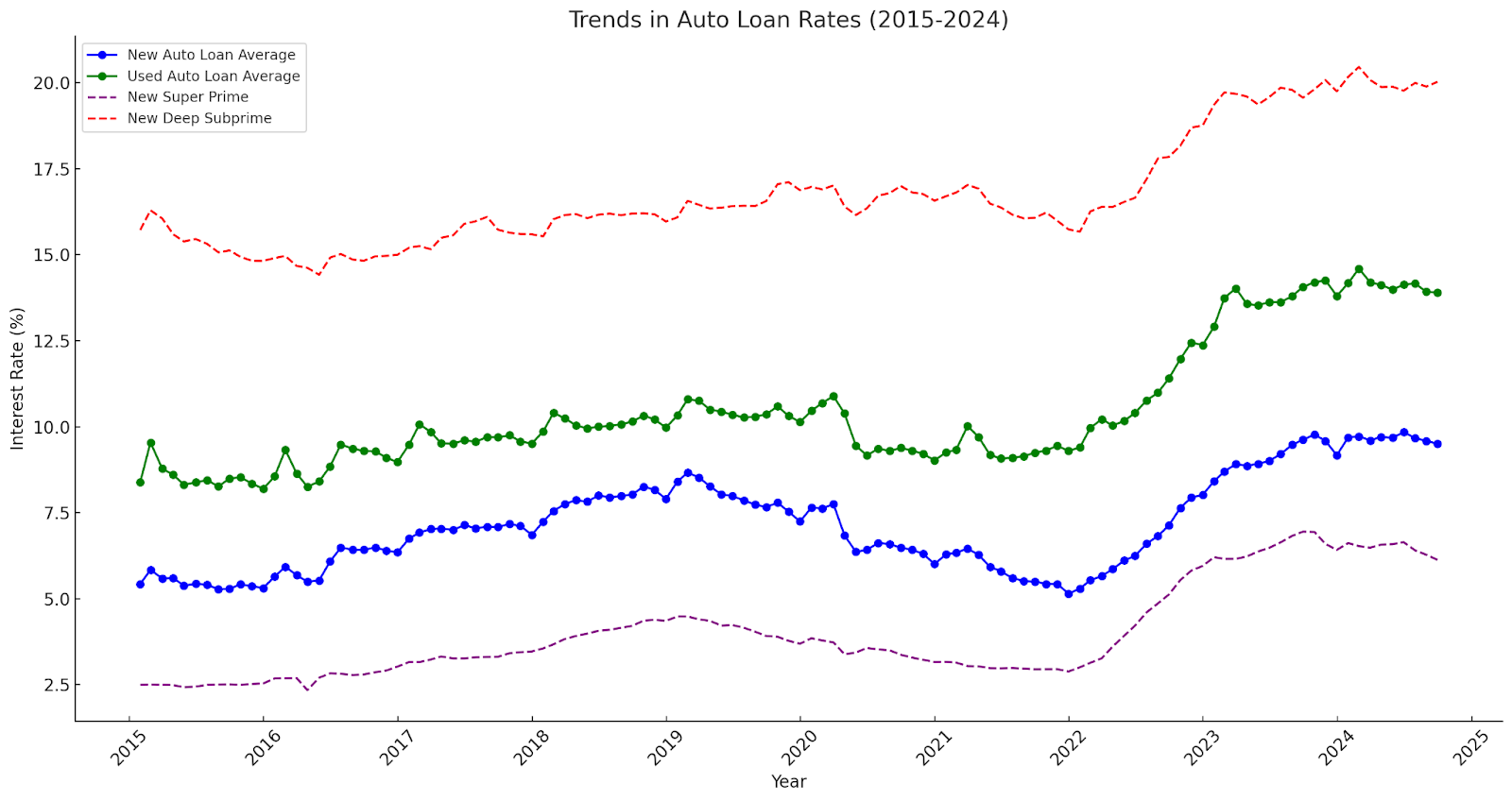

New car prices are still hovering above $48,000, with auto loan rates for prime (FICO: 660-719) customers typically falling between 7.5% and 10%. That’s driving monthly payments up to $740 — and once you throw in insurance, plenty of buyers are looking at well over $1,000 a month.

Source: Dealertrack

And so, dealership sales are being limited. 52% of the households said that they have delayed purchasing a new vehicle within the past year due to overall car ownership costs.

And it’s even worse on the used side of the business, where some of the most payment-constrained consumers in the subprime (FICO: <620) market have been hit especially hard.

I managed to catch up with Joel Bassam, President at Easterns Automotive Group, who told me that the large subprime market his stores serve is struggling to afford vehicles, making his group vulnerable to shrinking sales. Already, as an organization, his group misses 10–15% of car deals directly because insurance premiums are so high … 10-15%!

He said that in some cases, his customers were being quoted monthly premiums higher than the actual car payment. That's wild. And it begs the question…

When can we expect auto insurance premiums to come down?

The insurance experts I spoke to this week told me meaningful relief probably won’t be felt until late 2025 – 2026, largely because the auto insurance market is cyclical. It fluctuates between periods of soft and hard markets. Right now, things appear to be stabilizing, and some brokers believe we’re on the cusp of transitioning to a more favorable soft market.

And in some regions, auto insurers are already starting to file for rate reductions. According to the Swiss Re Institute, one in five personal auto insurance rate filings that took effect in the third quarter reflected a decrease.

In many cases, rate cuts are driven by competitive pressure, tech advances like A.I. and telematics, and segmentation strategies (i.e., bundling auto and home insurance policies). And again, these filings take months to get approved.

But business never stops, and people will always need cars, so…

Here’s how some dealers are tackling rising insurance premiums:

1) Structuring deals more creatively: Some dealers are using general sales strategies to lower monthly payments and free up the budget for insurance, like specifically hunting for vehicles with available tax credits and leasing rebates (used EV tax credits anyone?). Almost all dealers are also starting insurance discussions earlier in the sales process to set expectations (this should be obvious, but it isn’t!).

2) Embedding insurance into the sales process: A trendy solution in recent years has been integrating a digital auto insurance marketplace at the point of sale, where customers can get real-time quotes from multiple carriers. This helps customers find the most competitive rate on the spot — making it easier for them to commit to the insurance policy (and the car). Solid option for some.

3) Vertically integrating an insurance business: Larger, more sophisticated dealer groups are launching their own insurance arms. While this isn’t new — dealers have partnered in-store with companies like Allstate for years — many are expanding to offer more comprehensive insurance options. By capturing more sales margin via in-house insurance and profit from underwriting, they can subsidize lower premiums for customers to close deals on an as-needed basis. I like this play a lot, but it’s tougher to pull off unless a dealership has the bandwidth and resources to do it correctly.

And that’s where we stand. The market is slowly shifting, and we hope the worst of the insurance premium increases is behind us, as the past few years have been tough.

Dealers — what’s your strategy for handling rising premiums? Reply and share your thoughts. I’ll share some responses in the next edition of this newsletter.

SAB Capital is helping dealers unlock capital tied to their real estate through a dealership sale-leaseback. It’s a flexible option that lets you tap into the value of your property without giving up control of your business.

Here’s what a sale-leaseback offers:

Keep full operational control of your dealership

Enjoy fully deductible rent payments, providing tax advantages over interest payments from traditional CRE financing

Receive 1.25-2x the appraised value of your dealership

Benefit from competitive 100-150% loan-to-value ratios with costs similar to traditional lending

The proceeds can help fuel your growth, whether that’s expanding locations, upgrading facilities, or investing in future initiatives.

Curious to learn more? Connect with the team at SAB Capital today!

The business side of 70M+ recalled vehicles: What dealers are gaining

Inside the "Uber of car deliveries" — Moving 1.4M vehicles a year!

We’ve got tons of great jobs hitting the CDG Job Board right now:

Sheehy Auto Stores is looking for an Automotive Sales Manager in Richmond, VA.

Ron Marhofer Auto Family needs a Automotive Service BDC Manager in Ohio.

Riverside Auto Group is on the hunt for a Controller located near Rome, GA.

Looking to hire? Add your roles today—it’s 100% free.

Cowboy Toyota dealership sold to The CAR Group.

Ford announces $7,500 fleet discount on F150 Lightning.

Stellantis will soon test solid-state batteries in Dodge Charger EVs.

Ford Bronco sales slide unconcerning to dealers after 2 years of markups.

Qualcomm, Alphabet team up for automotive AI; Mercedes inks chip deal.

Did you like this edition of the newsletter?

Thanks for reading. See you on the next edition…

—Car Dealership Guy

Want to advertise with CDG? Click here.

Want to be considered as a guest on the CDG podcast? Right this way.

Want to pitch a story for the newsletter? Share it here.