Hey, everyone — Each week, we deliver two written recaps of the Car Dealership Guy Podcast, featuring the top 10 takeaways from each episode.

Get the key takeaways delivered straight to your inbox by voting below 🔽

—CDG

First time reading the CDG Newsletter? Subscribe here.

I can’t remember the last time the auto industry watched a Federal Reserve meeting as closely as it did last week. Collectively, we all breathed a sigh of relief as Fed Chairman Jerome Powell announced a 50 basis point cut (the largest in 16 years) to the benchmark interest rate. Now, the new range is 4.75% to 5%.

The obvious: Historically, as the Fed benchmark rate drops, so do auto loan rates… eventually. It won’t happen overnight and if/when auto loan rates drop, the change will likely be minimal. Let’s be real – no consumer will jump from a budget car to full-size pickup over a 0.5% cut.

But that doesn’t mean the auto lending environment won’t change.

Here’s what I’m watching closely —

1) Lenders will likely be slow to adjust auto rates

The Fed’s benchmark rate is not exclusively linked to auto loan rates, which tend to follow the “prime rate” (among other things). The prime rate is the interest rate that commercial banks charge their most creditworthy customers. While banks have begun trimming the prime rate (8%), they probably won’t be quick to give up charging higher financing costs.

Prime Rates published in The Wall Street Journal

Why? Commercial and Consumer Auto Finance expert Bill Ploog told me on a call this week that it really comes down to one thing: Lenders will attempt to maximize revenue in part by charging customers the highest possible interest rate while remaining competitive and staying within the law.

On top of that, car loan rates can take up to two months to reflect a Fed rate cut, as lenders wait for confirmation that lower rates will hang on before adjusting their offers, according to Cox Auto chief economist Jonathan Smoke.

State of play: Many Americans have been delaying vehicle purchases, hoping for lower prices, better interest rates, or the return of incentives. A Fed rate cut might not flood showrooms immediately, but it would likely nudge hesitant buyers into action.

Right now, the average interest rates for car loans are just below two-decade highs, averaging 9.72% for a new vehicle loan and 14.2% for a used one, according to Cox Auto.

The best shot buyers have at scoring lower interest rates is through automakers' captive financing arms like Ford Credit and GM Financial. Right now, deals are floating around at 2.99% to 3.99% APR, but with the Fed’s cuts, these lenders could slash rates even further, dropping them to a tempting 0.99% to 1.99% APR.

At the dealership, not a whole lot will probably change until a series of Fed cuts happen. Even though new car prices have cooled, they remain historically high, according to Cars Commerce.

The average new car payment is now around $740, far from the $400 payments most consumers can realistically afford.

And consumers with lower credit scores will likely continue to face high borrowing costs and stricter lending standards.

The real hurdle is getting shoppers approved for loans in the first place.

The meaningful change? Consumers now have cheaper options to tackle some forms of debt…

Are you still relying on auctions? We want to help you get out of this costly co-dependent relationship and start saving an avg. of +$2,700 per vehicle acquired with AccuTrade.

How? Tap into the stream of high-quality used cars that come through your service drive every single day. All you need to do is empower your team with a simple appraisal process that gives your customers instant, guaranteed offers.

Watch this demo to see how it works. Then, hear how the team at Germain Toyota has used it to avoid spending fees, shipping costs, and time at auctions for over 2 years. 🤯

According to LendingTree, 76% of people who asked for a lower credit card rate got an average reduction of 6.5 percentage points.

Additionally, a 14% consolidation loan could pay off a 20%-rate card, offering big savings. Balance transfer cards with 0%-APR intro periods are another way consumers can put cash back in their pockets for other purchases like cars or get their loans in good standing to refinance.

2) A potential refinancing surge

While it’s almost impossible to refinance an auto loan with negative equity and – no chance if it's delinquent – if an auto loan is healthy, refinancing can be a smart way to bring down the total cost of owning a vehicle over the term of the loan by paying less total interest.

Who will benefit the most? Likely prime borrowers (FICO: 660 - 719) who are perceived as more creditworthy and more likely to repay their loan. Refinancing a loan for a subprime (FICO: 580 - 659) borrower is a risker for lenders, and often, these borrowers have to jump through many hoops to get approved.

Of note: Refinancing isn’t always a smart move. Auto loans are amortized, so early payments mostly go toward interest. Refinancing late in the game might lower your monthly bill, but if you've already paid off most of the interest, you could end up paying more in the long run.

But for owners < 2 years into their loans, the savings could be substantial:

Using Bloomberg's auto refinance methodology and national average auto lending rates from bankrate.com, CDG internal data and insights analysts found that if prime borrowers who originated their loan at 8% - 10% APR in January 2024 were to refinance now, they could potentially shave between 0.25% - 2.25% off their new loan rate.

If we look at a loan balance of $35,000 originally financed at 10% and then refinanced at 7.75%, the difference in monthly payments is not much – about $40. But the real savings are closer to nearly $2,300 off the total interest costs. This potential to cut costs could drive a wave of refinancing activity among prime borrowers.

Yet – a potential “refinancing boom” could have negative consequences – especially from an investor perspective.

3) Increased risks to auto-backed securities

On the other hand, a surge in auto refinancing could spell bad news for auto-backed securities (ABS) investors.

ABS are basically bundles of auto loans that get sold to an issuer, who then turns them into tradable shares. It gives people a chance to invest in the returns on these loans, which are closely linked to interest rates.

But when consumers refinance their loans, auto interest rates go down – shrinking the yields investors could have made.

Yet – prime auto ABS issuance jumped 9.9% YoY to $57.5 billion a year to date, while nonprime issuance came in at $30.2 billion, up 17.5% YoY – driven by lenders’ need for liquidity and desire to fund more loans with the lowest possible cost of capital.

Digging deeper: Lenders find subprime customers to be the most profitable, particularly those who maintain their payments without refinancing (lowering interest rates). Despite higher delinquency rates, these loans are highly lucrative.

However, subprime borrowers face much higher interest rates, sometimes more than double what prime borrowers pay, leading to increased financial pressure.

Quick facts:

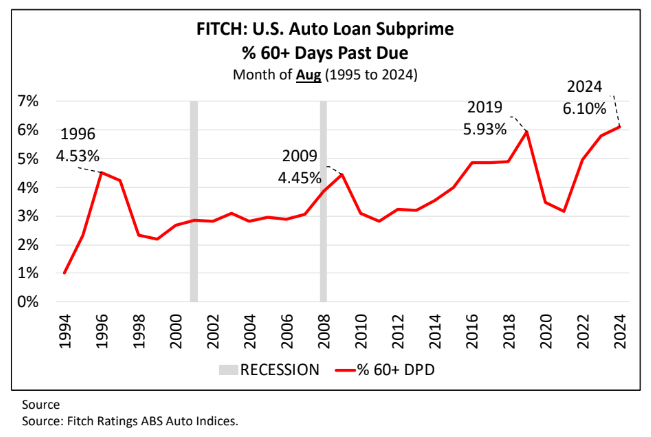

Subprime 60+ day delinquency rates hit an all-time high of 6.1% in August 2024, surpassing pre-pandemic levels, according to Ploog.

Subprime borrowers for new vehicles are borrowing nearly the same amount as prime consumers, averaging $40,900 in the second quarter of 2024, reports Experian.

Courtesy of Bill Ploog

Some lenders, like Exeter, are implementing high levels of auto loan modifications to avoid repossessions and keep auto ABS “healthy,” with a modification rate of 5.4%. This includes cutting interest rates and extending loan terms to give borrowers more breathing room. But there's a catch: interest keeps piling up during deferred payments, and it could take months just to get back to square one.

Looking ahead

The Fed signaled that it will cut the benchmark rate by another half a percentage point this year and expects four more cuts totaling 125 basis points in 2025.

But here’s the catch: Even with lower rates, if vehicle prices stay high, consumers might still find themselves priced out, especially as monthly payments remain well above what most can afford.

Next year’s rate cuts could reveal a harsh reality: Lenders may have to confront the deeper issue of how they assess credit risk – as interest rates alone won’t solve the gap between car prices and consumer budgets.

The story of Vince Sheehy: America's most interesting $2.5B car dealer!

The imminent evolution of A.I. in car dealerships: What to expect

We’ve got tons of great jobs hitting the CDG Job Board right now:

Sheehan Buick GMC is looking for a BDC Manager near Lighthouse Point, FL.

MotorEnvy is on the hunt for a Head of Operations in New Jersey.

Ron Marhofer Auto Family needs a Used Vehicle Buyer near Akron, OH.

Looking to hire? Add your roles today—it’s 100% free.

Why Hyundai and GM are teaming up in latest auto industry partnership.

VW prepares for ‘unprecedented’ UAW union negotiations in Tennessee.

With fewer prime used cars, dealers innovate.

Morgan Stanley cuts auto industry view to neutral, downgrades GM, Ford and Rivian.

Michigan Republican lawmakers write to Stellantis CEO Tavares about 'grave concerns'

Did you like this edition of the newsletter?

Thanks for reading. See you on the next edition…

—Car Dealership Guy

Want to advertise with CDG? Click here.

Want to be considered as a guest on the CDG podcast? Right this way.

Want to pitch a story for the newsletter? Share it here.