Hey, everyone. About that Super Bowl… It was a big year for car commercials—Kia, BMW, and Toyota all stuck out to me. My favorite had to be BMW, though. No surprise Christopher Walken drives a Beamer. 😂

—CDG

First time reading the CDG Newsletter? Subscribe here.

Today’s Biggest News

What’s Driving the Credit Availability Reversal?

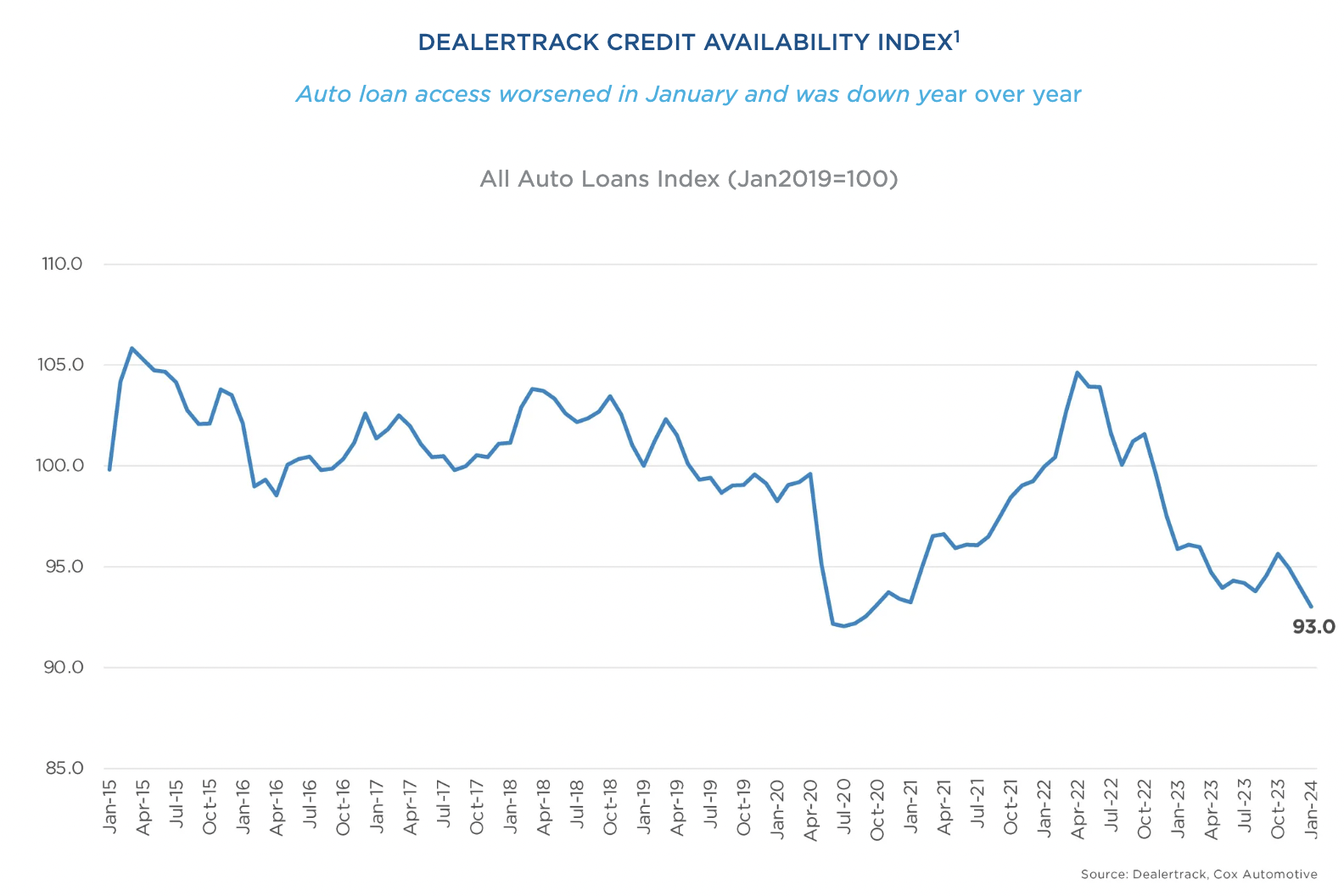

Major news for auto financing: Auto credit availability is now at its lowest point since August of 2020 after yet another monthly decline in January. In fact, credit access was tighter than a year ago in all channels and all lender types, according to Cox. Translation? Credit is tightening across all lender and customer types…not just subprime.

Via Cox

That creates a tough reality for consumers: Most credit availability factors moved against them last month, putting a chill on credit access…

The average yield spread on auto loans widened in January, meaning rates consumers saw on auto loans were less attractive in January relative to bond yields.

Term length, approval rate, and the share of subprime loans as part of the broader lending environment all declined.

Down payment amounts clocked in close to December’s rate—but still represented an all-time high. Super high down payments can deter customers from purchasing pricier models or even buying a car altogether.

As far as channels go, new vehicle loans tightened the most, while used vehicle loans through independent used dealers tightened the least.

And it’s hitting on the supply and demand sides of the lending equation: “Appetite to make consumer loans (credit card, auto & personal loans) remains very weak and suggests lending growth in this area, that is so important for consumer spending, will soon contract,” ING economist James Knightley wrote last week. Remember: Last quarter, banks reported considerably tightened lending standards (aka smaller credit limits, higher credit score requirements, etc.)

What that means: Consumers had a harder time getting an auto loan in January, especially for new vehicles. And last month continued a trend the auto industry has been grappling with for months…it’s not just expensive new cars keeping buyers on the sidelines. It’s also one of the most hostile financing landscapes in recent memory.

That’s a big part of why drivers are keeping their older models for longer…which means less business for dealers, directly impacting their bottom lines.

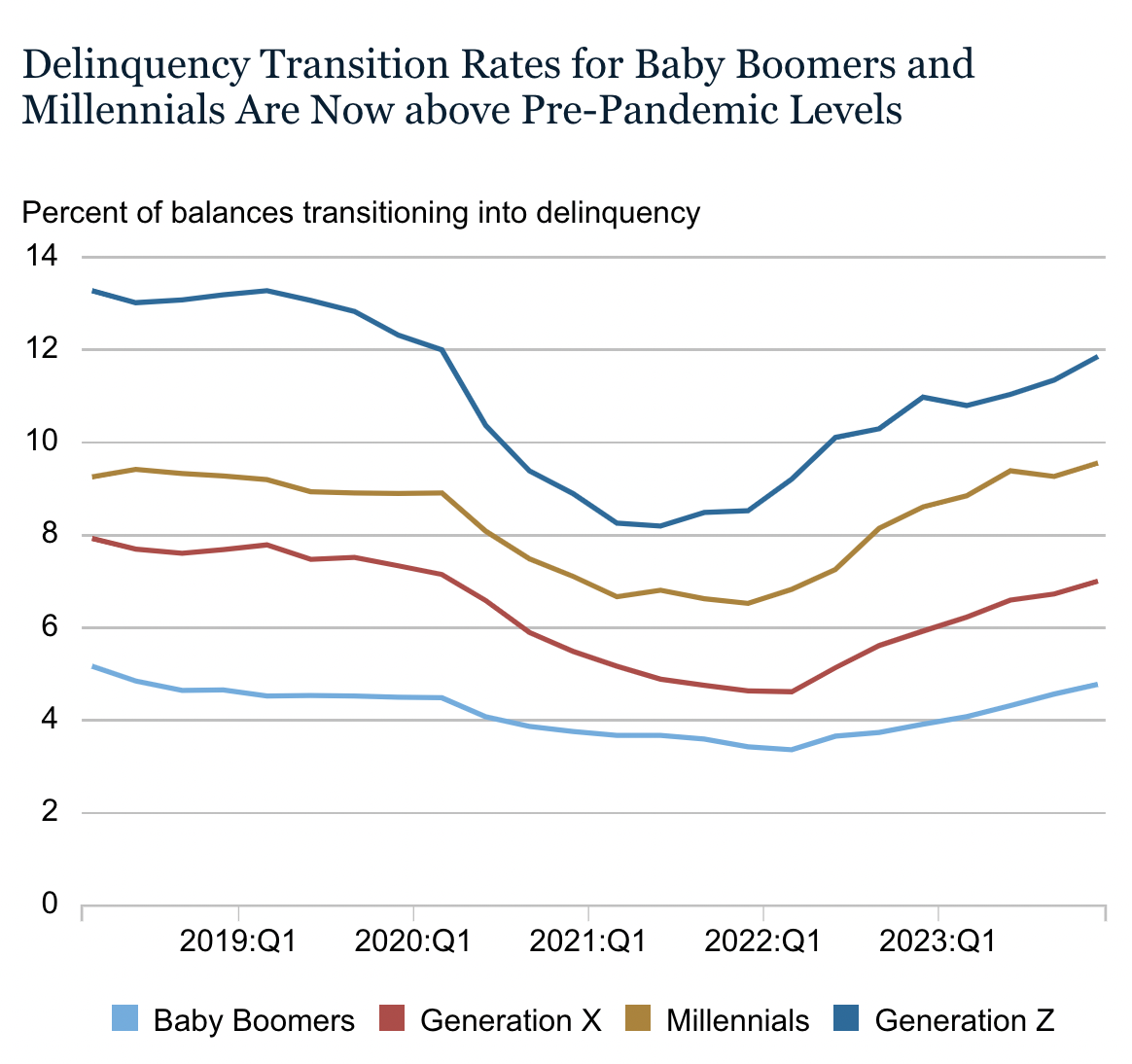

And it’s also a factor in rising delinquency rates. FYI, delinquency rates for most credit types have been rising after bottoming out in 2021 thanks to Covid-era forbearances on mortgages and federal student loans (plus those stimulus payments).

But now…things look like this:

Via the NY Fed

The Fed said delinquencies are on the rise across every age group and every income level, but especially among lower-income borrowers. About 2.2% of auto loan balances moved into delinquent status, or at least 30 days late, in Q4…the highest since at least 2017.

And the data suggest newer loans opened in 2022 and 2023 are performing worse than their older counterparts. Why? Maybe because car prices started skyrocketing during that time, forcing buyers to borrow more at higher rates.

But…there might be reason for optimism. Let me explain.

Several high-level executives at key auto lenders have suggested that 1) rising delinquencies and increasing barriers to auto credit are simply part of the normalization process post-pandemic and 2) we’ve already seen the worst of it.

Let’s roll the tape:

Capital One Financial’s Q4 auto loan delinquency rate of 6.3% remains below its pre-pandemic level of nearly 7%. Plus, the CEO said the industry has stabilized back to seasonal patterns in F&I.

Santander (whose US borrowers tend to skew more subprime) said that, before the pandemic, almost all of its borrowers who were 90+ days delinquent soon went into a charge-off. Now, though, it's closer to two-thirds. People are finding ways out of delinquency and avoiding repossession.

And Ally Financial said it expects auto charge-offs to peak by midyear.

So while the reality of lending is proving difficult for dealers, buyers, and banks alike…is there a case to be made for optimism? It seems like lenders think so. Do you?

Tell me: What do you expect for auto lending through 2024?

This Week’s Episodes of the CDG Podcast

Anyone who succeeds in the auto world has to be a chameleon. With how fast things change, evolution and reinvention are part of the job description. So how does Chad Brooks, Head of Dealer Development at Valvoline, roll with the punches? He gave me the full rundown, plus his POV on how dealer service departments need to keep pace with a changing automotive reality, in this packed episode of the CDG Podcast.

Listen to the episode here, and subscribe to the CDG Podcast on Apple, Spotify, or wherever else you get your podcasts. And thank you to CDK Global and Valvoline for making this content possible.

Together with Cars Commerce

You know your store’s reputation is essential to the health of your business—but do you know how to diagnose it? ⭐️🩺

With so many reviews to read through, it's not easy to identify which specific aspects of your experience are resonating well (and not so well) with your customers.

Dealers: Check out your Cars Commerce Experience Report. 📊👀

This free report measures and tracks customer sentiment for each aspect of your experience—from lead follow-up to financing—and helps you benchmark those perceptions against your local market and OEM averages.

Improve your experience. Build your reputation. Promote what makes you different. It all starts with using data to diagnose where you are today.

In Other News

Your POV on affordability. Last week, I wrote about the affordability crisis that’s slamming the auto industry (read here if you missed it). I asked all of you what you thought, and your perspectives were really insightful. Here are some highlights:

“My family just bought a new Sienna. Even with good financials we’re still paying a ton. We plan to keep it for as long as possible (15+ years). But it makes me wonder when loans will be extended. I would have taken longer terms for a lower payment. And banks would make more money in interest if they did that. Seems like a win-win for everyone (even though paying more interest isn’t ideal).”

“One thing I observed all through the early 2020s is dealer markups and bogus ‘dealer-installed options’ jacking up prices out of pure greed. Sure, I get that when cars were scarce dealers needed to survive and keep the lights on, but once the supply chains were back in decent shape and inventories began to recover, Hyundai, Toyota and Honda, for example, still couldn't bear the thought of dropping the $5k or more ADMs and $1k paint protection packages. So at least part of the affordability problem is due to dealers' pricing policies, and not just the manufacturers dropping base models and loading up on high margin trim levels.”

“I’m making my 2010 Ford with 220,000 miles run ’til the wheels fall off. Literally. I’m paying off other debt and cannot afford a $600/month payment with 8% interest for something used with 100,000 miles.”

“I dealt with the issue by selling my 2004 Toyota Highlander and moving to New York City, lol. I'll only ever spend at most $34/week on transportation (the cost of a week pass on the MTA) if I only use public transport.”

Thanks for sharing your thoughts. You rock.

Highlights from the CDG Job Board

We’ve got tons of great jobs hitting the CDG Job Board right now. Here are some standouts for anyone looking for their next move.

Want to go into sales? We’ve got an Inbound Business Development Rep at VETTX or an Account Executive at Edmunds in Palm Beach.

Interested in the startup world? Cairo (value prop: digitizing vehicle titles) is looking for a VP of Business Development in NYC.

Looking for a great dealership position? Become an VP of Fixed Operations at Norm Reeves Auto Group in California.

Looking to hire? Add your roles today—it’s 100% free.

The Backlot

This is my tried and true method for finding and hiring the best auto technicians.

Ford has set a target of cutting $2 billion in costs to improve profitability. Bloomberg has a look at what they’re cutting to make it happen (so long, automated parallel parking).

Apple went deep on autonomous vehicle testing last year. 👀

Hyundai is exploring a $3 billion IPO for its India unit. If all goes to plan, the business could be valued at $30 billion.

This Texas dealership is recruiting college athletes for its marketing. Pretty smart, if you ask me.

The latest in EV charging infrastructure: Stellantis is joining Tesla’s network, while seven other automakers are forming their own standard called “Ionna.”

Thanks for reading. Got an idea for something you’d like to see in this newsletter? Hit reply and tell me more. I’d love to hear from you.

See you next time. ✌️

—Car Dealership Guy

Did you like this edition of the newsletter?

Want to advertise with CDG? Click here.

Want to be considered as a guest on the CDG podcast? Right this way.

Want to pitch a story for the newsletter? Share it here.