Hey, everyone. You know what they say about ambitious businesses…you have to eat your own dog food. Well, here we are.

I’m hiring our first Data & Insight Analyst at Car Dealership Guy — and the role is officially posted on my job board. We’re bringing on a team member to help source, contextualize, and deliver the most powerful and up-to-date data to me and my team. It’s a role with huge potential. Want to apply? Go here.

—CDG

First time reading the CDG Newsletter? Subscribe here.

Today’s Biggest News

One Way to Stop the Auto Lending Spiral

Auto lending is going through a moment right now.

Car prices and interest rates are both still high…which makes it harder for borrowers to make their monthly car payments…which introduces risk to the lending ecosystem…which has forced banks to tighten credit standards…which ices out subprime borrowers who can’t fork over a big down payment…which hamstrings sales for dealers…which—you get it.

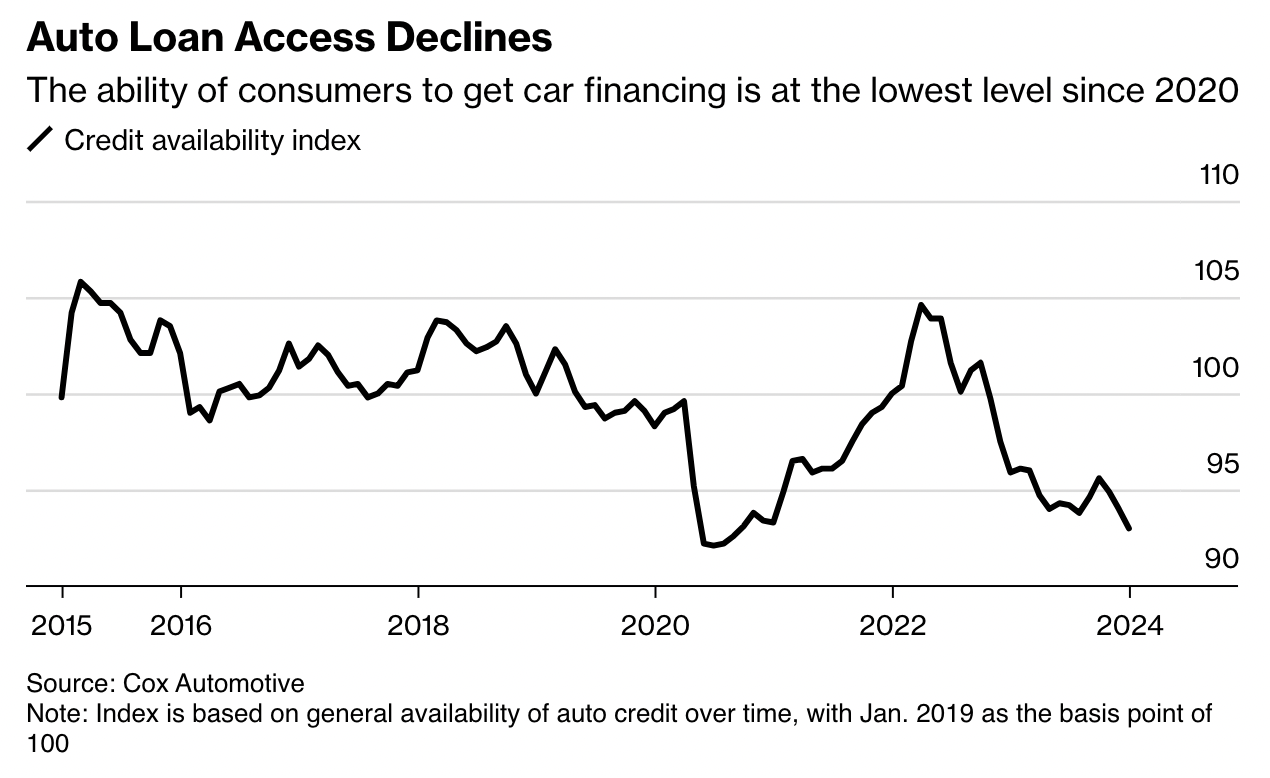

We’re in a tough cycle. Access to auto credit is the lowest it’s been since August of 2020.

Via Bloomberg

But for all the ink that’s been spilled (and tweets that have been sent) about the current state of auto lending, I think there’s one interesting path to follow that could pull us out of this cycle…and it has to do with a changing lender playbook.

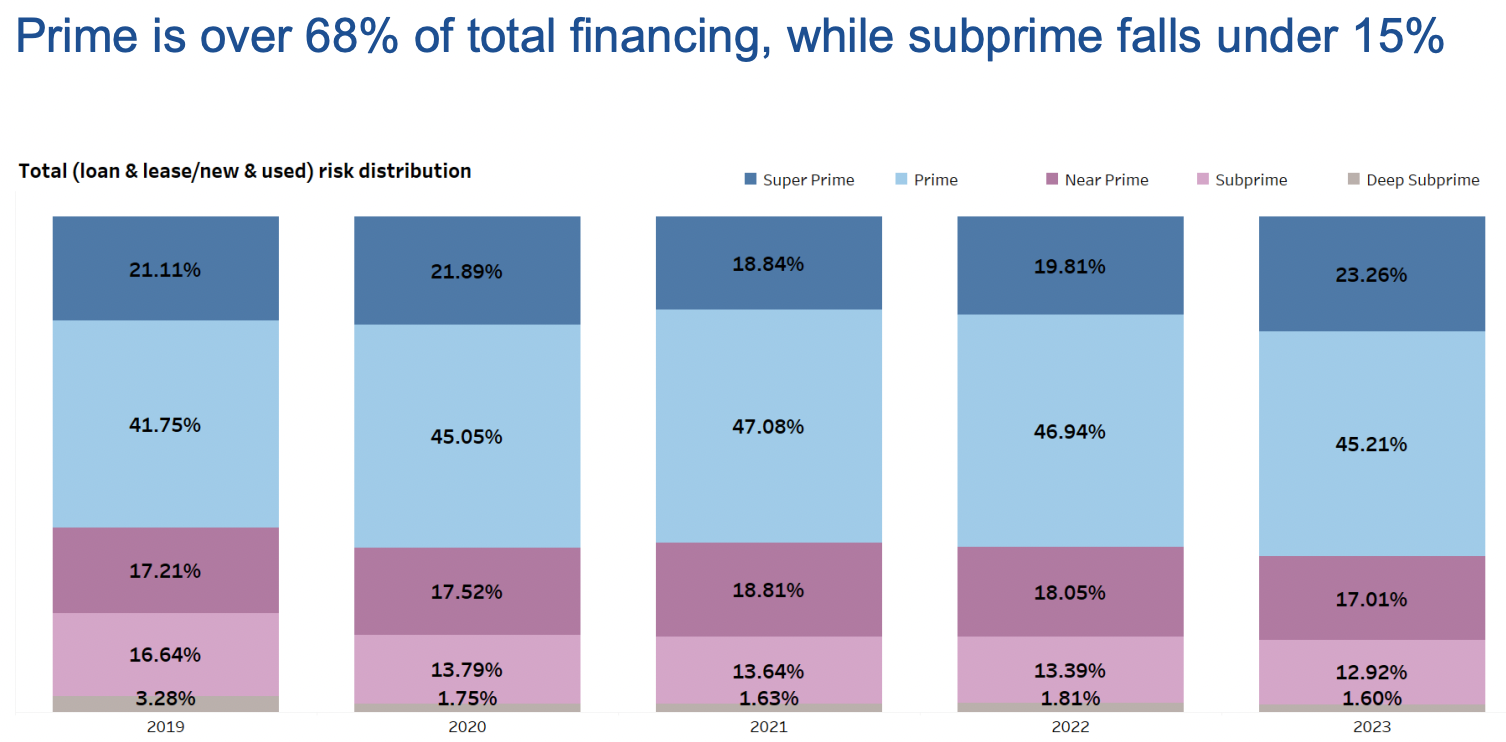

Let me explain. It starts with understanding that borrowers with lower credit scores are losing access to financing (which can impact a lot in our industry, including used car sales volumes). In fact, half of Americans who applied for loans in the past two years were turned down, according to Bankrate.

And it’s not new. I posted this almost a year ago, and circumstances haven’t changed a whole lot:

So why are subprime borrowers being pushed out? The average credit score in the US only rose by one point last year…so it’s not as if we’re all getting better monthly credit reports.

Instead, it’s likely because lenders are restricting financing to combat higher interest rates and hedge increased portfolio risk—that means loans cost more + it’s harder to get one in the first place.

Via Experian

And it’s worth noting: Delinquencies are on the rise at the same time, especially in lower income areas, according to the Fed. The percentage of US auto loans 90+ days delinquent rose well above pre-pandemic levels to 2.7% last quarter. The 15-year average is just 2.2%.

Part of why that could be? The average monthly payment on a new car loan rose to $623 in Q4—the highest ever, even as car prices are falling.

The average auto loan rate was 9.2% for a new car and 13.8% for a used car at the end of 2023.

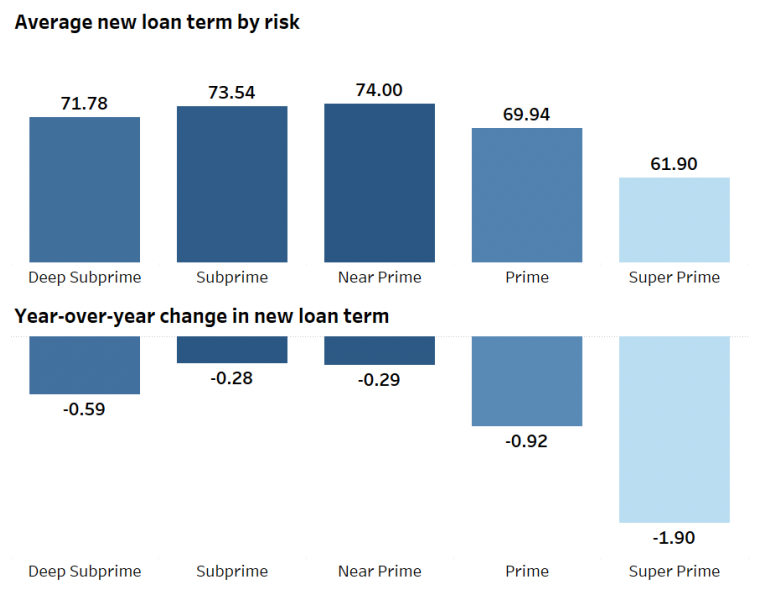

So…the F&I strategy is changing. Longer loans with lower monthly payments (the traditional model) can lead to more negative equity and drivers getting stuck with unreliable and old cars. Longer terms also carry a higher risk of default, so those rising delinquency rates make lenders apprehensive of those long-term loans.

Instead, lenders are doing something different: suggesting shorter terms and higher monthly payments for qualified drivers. Check this out:

Via Experian

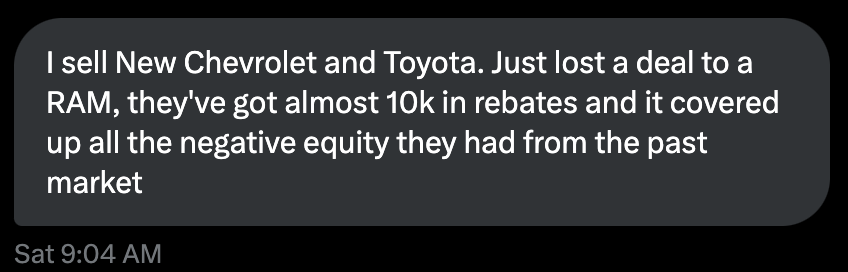

And manufacturers are playing a part in the strategic shift, too. For the first time in several years, we’re seeing significant discounts on certain vehicles.

Stellantis (Chrysler, Dodge, Jeep, Ram, etc) is now offering up to 10% or 15% discounts on some models, for example.

Days supply of new vehicles at the beginning of February was a relatively high 80 days. And higher inventory could mean more incentives and discounts.

The other key? Rebates. Take a look at this message I recently got from a CDG follower:

Better incentives + strong rebates = opportunity, especially for drivers with lower credit scores who wouldn’t otherwise qualify for financing. Why? The lenders are taking less risk on the collateral when it costs less to begin with.

And LTV ratios tell us this is a trend to watch. The LTVs, or loan to value ratios, are typically lower when manufacturers are hitting rebates hard. Want to take a guess what’s going on with LTVs right now?

They’re falling, for both new and used models, according to Experian.

So…maybe there’s a way out after all. A means for borrowers of all kinds to get the financing they need to buy the cars we want to sell them. Tell me what you think—and what you’re seeing on the dealership floor—in the replies.

This Week’s Episodes of the CDG Podcast

Want a masterclass in business leadership? Listen to my conversation with Brian Benstock, Partner and General Manager of Paragon Honda & Acura. My promise to you: A full rundown of how Brian built the #1 Honda dealership in the world, the secret to his wildly successful 24-hour service center, and tons of insight on the industry, from how leasing could solve the affordability crisis to career development in the auto world. Don’t miss it.

A tough break doesn’t have to break you. Ryan Maher, former infantry officer and now CEO of BizzyCar, was inspired to start his business during the toughest months of the Covid-19 pandemic. In this inspiring episode, he shared with me a ton of insightful ideas about consumer behavior and the ins and outs of massive recalls. This is an epic one.

Listen to the episodes here, and subscribe to the CDG Podcast on Apple, Spotify, or wherever else you get your podcasts. And thank you to Cars Commerce, AutoFi, Private Auto, CDK Global, and BizzyCar for making these episodes possible.

Together With Cars Commerce

You know your store’s reputation is essential to the health of your business—but do you know how to diagnose it? ⭐️🩺

With so many reviews to read through, it's not easy to identify which specific aspects of your experience are resonating well (and not so well) with your customers.

Dealers: Check out your Cars Commerce Experience Report. 📊👀

This free report measures and tracks customer sentiment for each aspect of your experience—from lead follow-up to financing—and helps you benchmark those perceptions against your local market and OEM averages.

Improve your experience. Build your reputation. Promote what makes you different. It all starts with using data to diagnose where you are today.

In Other News

Nissan is getting back into fleet sales. In February, Nissan sold nearly 40,000 vehicles (aka 44% of its total volume) to fleet, per Auto News. A year ago, the fleet share of overall sales was about 25%.

Dealers aren’t super thrilled—this move floods the market and lowers residuals for Nissan dealers. And lower residuals = less value for consumers.

Nissan dealers—how concerned are you about this? Hit reply and tell me what you think.

Highlights from the CDG Job Board

We’ve got tons of great jobs (in addition to our own) hitting the CDG Job Board right now. Here are some standouts for anyone looking for their next move.

Always loved working in client-facing roles? VETTX is looking for a client success manager.

Got the drive to develop a tech-forward startup’s market across the US? Fullpath is looking for a regional sales manager in Florida and Georgia.

Think you’d be great at keeping people safe and businesses working efficiently? KPA is looking for an automotive finance risk management consultant.

Looking to hire? Add your roles today—it’s 100% free.

The Backlot

Nissan is reportedly in advanced talks to invest in struggling electric vehicle maker Fisker—offering it a potential financial lifeline.

The number of US new car dealerships fell slightly in 2023, but throughput (aka the average new vehicle sales per franchise) jumped.

The SEC charged Lordstown Motors with misleading investors by exaggerating the sales outlook for its Endurance full-size electric pickup truck.

Lower inflation on key material prices has helped auto suppliers’ bottom lines. But…they’re expecting costs to climb on labor post-UAW strike.

The IIHS has new scoring criteria for one of its crash tests. The new standard changed the crash test ratings on 13 vehicles.

February sales rose year-over-year for Honda, Hyundai, Mazda, and Subaru. Kia? Went in the opposite direction.

Thanks for reading. Got feedback on this edition? Hit reply and tell me more—I’m always looking to level up. See you next week.

—CarDealershipGuy

Did you like this edition of the newsletter?

Want to advertise with CDG? Click here.

Want to be considered as a guest on the CDG podcast? Right this way.

Want to pitch a story for the newsletter? Share it here.