Hey, everyone — Three-year-old lease returns are typically the best-selling cars at the wholesale level but they’re about to become more scarce. Cox Auto analysts forecast a 12% drop in lease maturities for Q3 and steeper declines of 17-18% in Q4.

Why? Fewer cars produced and sold during COVID means fewer cars are hitting the secondary market and with residual values trending down, the best deal for many consumers is to buy out their lease. Whatever the reason — supply is about to get tighter and used car prices will likely go up.

—CDG

First time reading the CDG Newsletter? Subscribe here.

Remember when I mentioned that a lot of the questions I get are about auto lending? Well, I've been getting even more lately…

Here's the deal: Car buyers and dealers are really feeling the pinch from crunched lending conditions. Everyone's wondering if interest rates will stay high, whether or not subprime lending approvals will tighten further, or if some lenders might quit offering auto loans altogether.

This got me thinking about where auto lending is today and where it could be headed.

Post-pandemic, auto loan approvals have been unpredictable. After a brief surge in 2021, fueled by strong credit scores and stimulus money, supply chain issues have now constrained both car supply and loan demand. Today, rising costs are putting the brakes on car loans. Lenders are more selective, too (more on that later). For many families, the dream of owning a new car is slipping away, replaced by the harsh reality of high monthly payments and stringent loan conditions.

The details: Total auto loan debt grew to $1.6 trillion, but new loan originations (5.8 million in Q1) are still down from pre-pandemic levels. To give you an idea, that’s 1.7 million fewer auto loan originations than in Q3 2019 - a pretty meaningful drop.

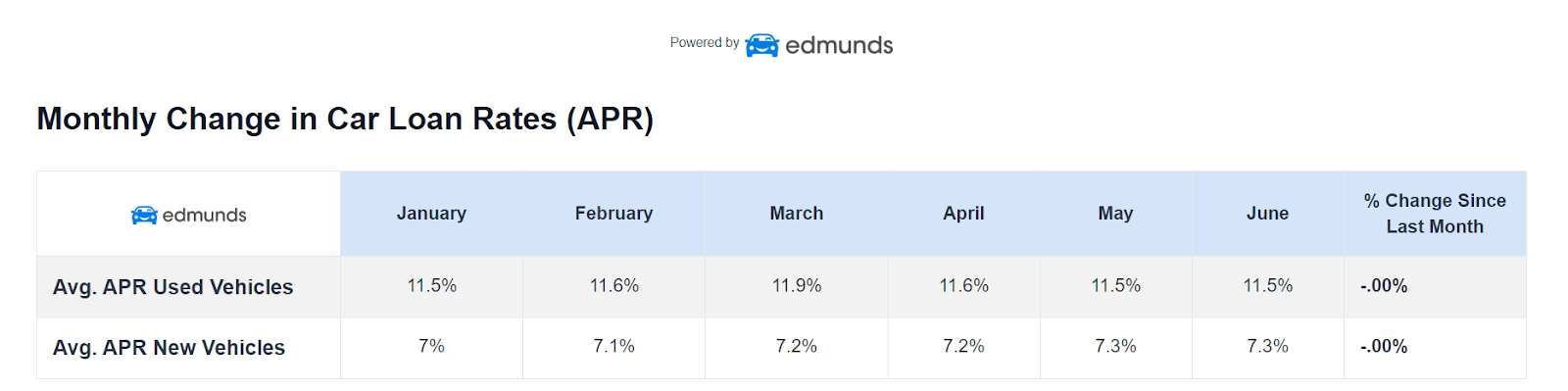

The reason originations are down? You guessed it… average auto loan interest rates (new, 7.3% and used, 11.5%), elevated vehicle costs, and longer loan terms are the primary culprits pushing loan balances up and keeping many would-be car buyers on the sidelines.

So, why have lenders tightened up? – There are a few reasons

1. First, the obvious: Negative equity – With more new cars available, used car values have plummeted. The Manheim Index, a key indicator for used car prices, is down 8.9% in June compared to last year, sitting at 196.1. June marks another month of decline that began in 2021, but analysts are optimistic that “the decline may be nearing its floor.”

For context: Prices in the three-year-old used vehicle market dropped by 1.5% last month. Before the pandemic (2014-2019), prices fell on average, 0.5% in the four weeks of June. Meaning, that cars are depreciating substantially faster today than long-term averages.

So, car buyers who bought new vehicles at high MSRPs during the pandemic have seen a big drop in their vehicle’s value — ending up “underwater” on their loans.

These negative equity situations are becoming increasingly common, with upside-down trade-ins rising to 23.9% in Q2.

This can make getting a new loan difficult and trap consumers in a cycle of debt. When this happens, repossessions become twice as likely if negative equity is involved (within two years of taking on a new loan) and can substantially affect credit history and prevent consumers from getting financing in the future.

Are you still relying on auctions? We want to help you get out of this costly co-dependent relationship and start saving an avg. of +$2,700 per vehicle acquired with AccuTrade.

How? Tap into the stream of high-quality used cars that come through your service drive every single day. All you need to do is empower your team with a simple appraisal process that gives your customers instant, guaranteed offers.

Watch this demo to see how it works. Then, hear how the team at Germain Toyota has used it to avoid spending fees, shipping costs, and time at auctions for over 2 years. 🤯

2. Subprime and Near Prime concerns – Lower credit scores --> more risk for lenders --> higher interest rates and (you guessed it) larger bank fees for dealers! For our friends new to the term "bank fee," it refers to the payment dealers make to lenders for writing a "risky" loan, which helps lower the loan-to-value ratio.

But in some rare cases, banks and lenders are stepping away from auto loans altogether.

Since the start of 2023, Citizens Bank scaled down its auto loan portfolio from $14.5 billion in 2021 to $5-$6 billion by 2024.

Rifco National Auto Finance, a major subprime lender in the Canadian car market, has put all auto lending on hold for an indefinite period of time.

3. Loan amounts and terms – Even buyers with good credit scores are struggling to finance a luxury or high-end car. It's all about risk—the bigger the loan amount, the more chances something could go wrong.

The average monthly payment for new vehicles in 2023 was $729, which is a 24.4% increase from 2022.

The average monthly payment for used vehicles was $528, which is a 1.7% increase from 2022.

Lenders are also extending loan terms to make cars seem more attainable. The average new and used car loan now lasts 5.5 years (67.6 and 67.4 months, respectively). This might make monthly payments more manageable, but significantly more interest is paid over the loan's lifetime.

4. Delinquencies – 4.4% of auto debt was at least 90 days late in the first quarter of 2024. This is up 13.4% from the first quarter of 2023 and a whopping 32.83% over the past decade, says the New York Fed. Meanwhile, the percentage of auto loans that fell to 30 days past due was 7.9% in the first quarter of this year, up from 6.9% in the first quarter of last year.

In response, lenders (in many cases) are tightening their underwriting criteria to safeguard profits. Carvana, for example, is requiring higher down payments from customers and placing limits on maximum payments.

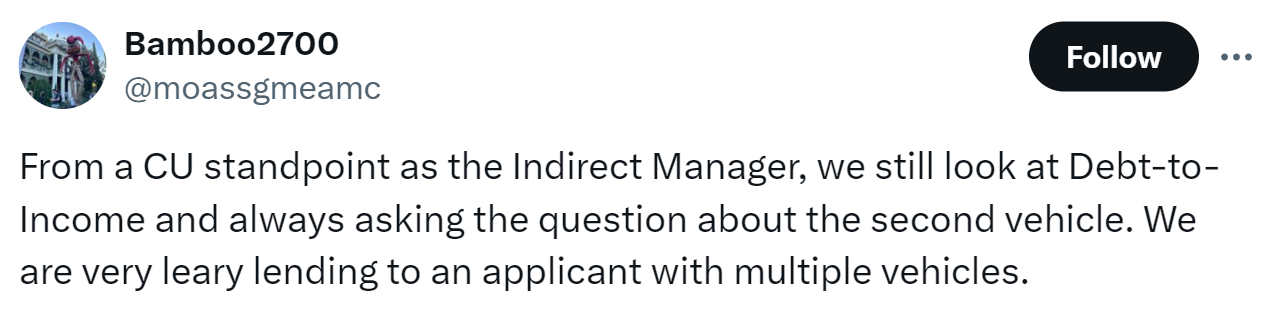

One of my followers on X, @moassgmeamc, pointed out what else lenders are watching for…

So, the big question is: what happens next?

We know that dealers want to sell cars, and people want to buy them. Lenders, dealers, and manufacturers need to work together to make this happen.

Moving forward, I expect a few things…

1) It seems increasingly likely that interest rates won’t change much until after the election, which will continue putting pressure on dealership cost structures (floorplans, anyone?) and overall consumer demand.

2) Automakers will continue subventing rates / increasing incentives to drive sales in an environment with growing inventories and cooling consumer demand.

3) As “cash deals” remain a more common occurrence in a post-ZIRP world, F&I offices will likely have a harder time maintaining revenue streams and look to introduce new products (in addition to optimizing attach rates on existing products).

And likely much more... But for now, we wait patiently. If the past few years have taught us anything, it's that the auto industry is always full of surprises.

The car ad maverick: Secrets to dealership profitability - In this episode Len Short, Chairman and CEO at Lotlinx, shares how his company became a major player in retail automotive, discusses strategies for reducing carryover inventory, and shares insights into the current market landscape.

The dealership mogul: Leading a $2B dealer group - Last week, I got to speak with Aaron Zeigler, President of Zeigler Auto Group. We talked about what it takes to lead a $2 billion dealer group, how anyone can run a $100 million business, addictions in the dealership, and the potential consequences of November’s election.

Listen to the episodes here, and subscribe to the CDG Podcast on Apple, Spotify, or wherever else you get your podcasts. And thank you to Cars Commerce, Withum, Lotlinx, and Auto Hauler Exchange for making these episodes possible.

We’ve got tons of great jobs hitting the CDG Job Board right now. Here are some standouts for anyone looking for their next move.

Want to take your auto sales experience to the next level? Ron Marhofer Auto Family is looking for a general sales manager near Akron, OH.

Have a knack for helping businesses grow? OPENLANE is seeking 10 market sales managers all across the country.

Are you a B2B sales pro? Edmunds is looking for an account executive located in Riverside, CA.

Looking to hire? Add your roles today—it’s 100% free.

Akio Toyoda's $10 million compensation broke a company record.

Ford unveils new Capri EV with nearly 400 miles range and sports car performance.

A rare piece of Tesla history is up for auction.

BMW is recalling more than 394,000 cars because airbags could explode.

Volkswagen cuts 2024 sales margin forecast on possible Audi EV-plant closure.

Did you like this edition of the newsletter?

Thanks for reading. See you on the next edition…

—Car Dealership Guy

Want to advertise with CDG? Click here.

Want to be considered as a guest on the CDG podcast? Right this way.

Want to pitch a story for the newsletter? Share it here.